From Debt to Dreams: Your Roadmap to Financial Freedom with Dream Inc

3/29/202510 min read

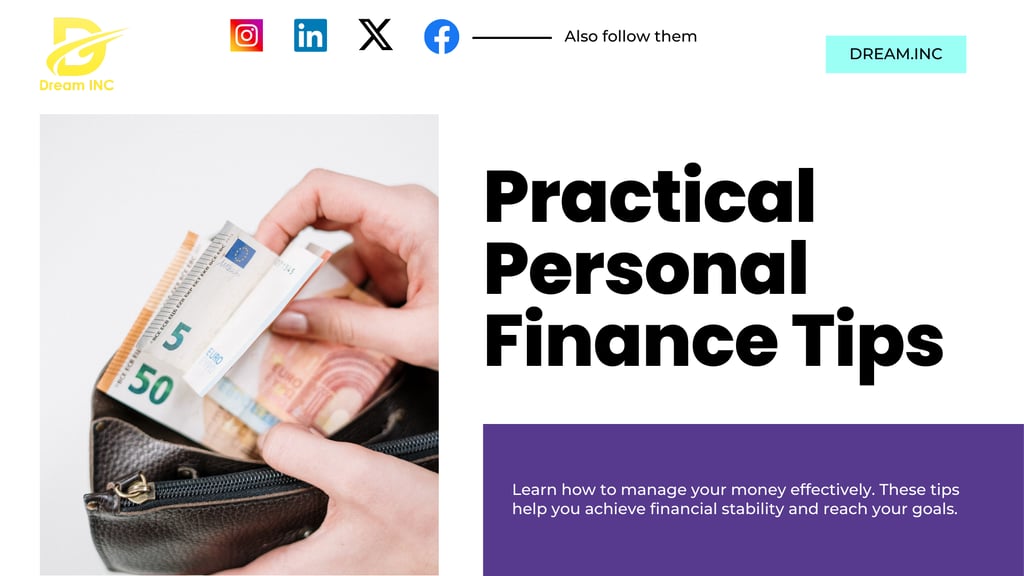

Understanding Financial Freedom

Financial freedom is often described as the state of having sufficient personal wealth to live without having to actively work for basic necessities. It is achieved when an individual's investments generate a residual income that covers their living expenses. This concept extends beyond merely eliminating debt; it encompasses the ability to manage finances in a way that aligns with personal aspirations and life goals.

Many people hold misconceptions about financial independence. Some believe it simply means being rich or having a high income. In reality, financial freedom is more about effective money management and making informed choices about spending, saving, and investing. It is not exclusively reserved for the wealthy; rather, it is accessible to anyone willing to commit to financial education and disciplined fiscal habits. By creating a budget, reducing unnecessary expenses, and establishing an emergency fund, individuals can take substantial steps toward achieving this coveted status.

Achieving financial freedom can lead to a fulfilling life, allowing individuals to pursue passions, travel, invest in hobbies, and provide for their families without the stress typically associated with financial instability. The pursuit of financial independence fosters a sense of empowerment and control over one's own life, enabling people to make choices that resonate with their values and long-term aspirations.

As individuals embark on this journey towards financial freedom, they may find that it enhances their overall well-being. Financial independence serves not just as a checklist item, but as a lifestyle choice that promotes personal growth. The ability to make decisions uninhibited by financial constraints opens up a world of opportunities, fostering a mindset geared toward continuous improvement and fulfillment.

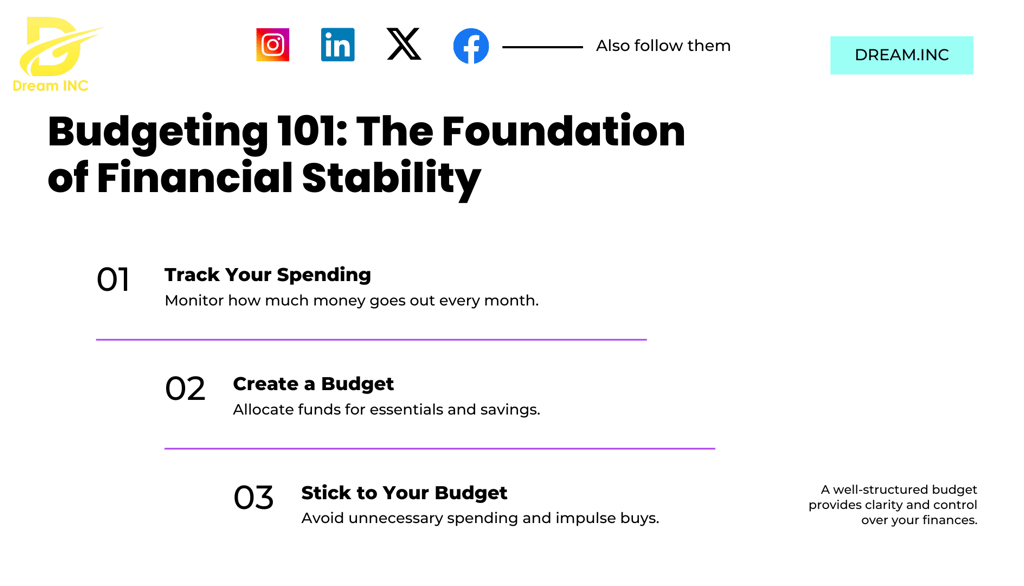

Step 1: Lay the Foundation with Budgeting

Budgeting is an essential component of achieving financial freedom, serving as the foundation upon which individuals can build their economic goals. By effectively managing income and expenses, a budget provides clarity and direction towards achieving one's financial aspirations. To create a practical budget, it is first necessary to assess all sources of income and consider every expense, both essential and discretionary. This initial evaluation helps individuals understand where their money is going and enables them to make informed decisions regarding their finances.

One effective method for budgeting is the envelope system, which involves allocating specific amounts of cash for various spending categories. Each category is assigned an envelope, and once the cash for that category is spent, no further expenditures can be made. This tangible approach can help individuals develop self-discipline in their spending habits and prevent overspending. Another popular method is zero-based budgeting, which focuses on assigning every dollar of income a specific purpose, ensuring that all expenses are covered, and creating a surplus for savings or debt repayment. This method encourages a proactive approach to managing finances, as every dollar is accounted for, leaving no room for frivolous spending.

Tracking spending is crucial in both methods, as it helps individuals monitor their financial behavior and adjust their budgets as necessary. By regularly reviewing their income and expenses, they can identify patterns and areas where savings can be made. Setting financial goals, whether short-term or long-term, is also integral to the budgeting process. Clear goals motivate individuals to stick to their budgets and prioritize saving or debt reduction. By laying a solid foundation with effective budgeting techniques, individuals position themselves favorably on their journey from debt to dreams and ultimately towards financial freedom.

Step 2:Strategies for Debt Reduction

Reducing and eliminating debt is a critical step on the journey to achieving financial independence. There are several strategies that individuals can employ to tackle their debts effectively, with two popular methods being the snowball method and the avalanche method. The snowball method focuses on paying off the smallest debts first, leading to quick wins and boosting motivation. As each small debt is eliminated, the individual gains confidence and a sense of accomplishment, which can provide the impetus to tackle larger debts over time.

On the other hand, the avalanche method prioritizes debts with the highest interest rates, which minimizes the total interest paid over time. This approach can save money in the long run and may be more suitable for those who are mathematically inclined and want to optimize their repayment process. It is important to carefully evaluate personal financial situations and choose the method that resonates most with individual preferences and goals.

Besides these methods, debt consolidation is an option worth considering. This approach involves combining multiple debts into a single loan with a lower interest rate, simplifying monthly payments and potentially reducing the repayment period. However, it is essential to understand the terms of any consolidation offers and ensure that they do not inadvertently lead to further financial dilemmas.

Addressing the psychological aspects of debt is equally important. Debt can be a source of stress and anxiety, impacting mental health and decision-making. To cope with these challenges, setting realistic and achievable financial goals can help maintain motivation during the repayment journey. Additionally, seeking professional advice from financial counselors can provide tailored strategies and support. Whether through advice, budgeting assistance, or emotional coping mechanisms, professionals can play a critical role in navigating the complex landscape of debt reduction.

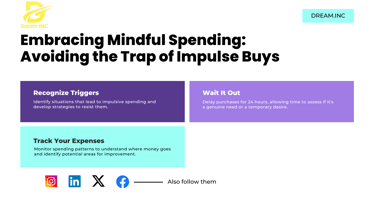

Step 3: Mindful Spending Practices

Mindful spending is an essential component of achieving financial freedom, as it encourages individuals to reflect critically on their purchasing decisions. This practice involves distinguishing between wants and needs, fostering a discipline that prevents impulsive purchases while enhancing overall financial responsibility. By adopting mindful spending techniques, individuals can create a more stable and secure financial future.

To differentiate between wants and needs, individuals must first assess the purpose of each purchase. Needs are essentials that are fundamental for daily living, such as food, shelter, and healthcare. Conversely, wants are non-essential items that may provide temporary satisfaction, such as luxury goods or entertainment options. Creating a list of these categories can help clarify priorities and encourage more intentional spending choices.

One effective strategy for practicing mindful spending is to implement a waiting period before finalizing any non-essential purchases. This delay allows individuals to reconsider the necessity of the item, preventing the influence of fleeting emotions or marketing pressures. Additionally, keeping a detailed spending journal can prove beneficial, as it offers insight into spending habits, helping to identify patterns that may need adjustment.

Cultivating a mindset that prioritizes value over volume is vital for mindful spending. Rather than focusing on acquiring numerous items, individuals should concentrate on investing in high-quality products that possess long-lasting value and better serve their needs. This approach not only enhances satisfaction but also reduces the frequency of purchases, which can lead to improved financial stability.

Practical tips for examining purchase decisions include asking oneself key questions, such as “Will this enhance my overall wellbeing?” and “How often will I use this?” By embracing these mindful spending practices, individuals can foster a healthier relationship with money, ultimately paving the way to financial freedom and the pursuit of their dreams.

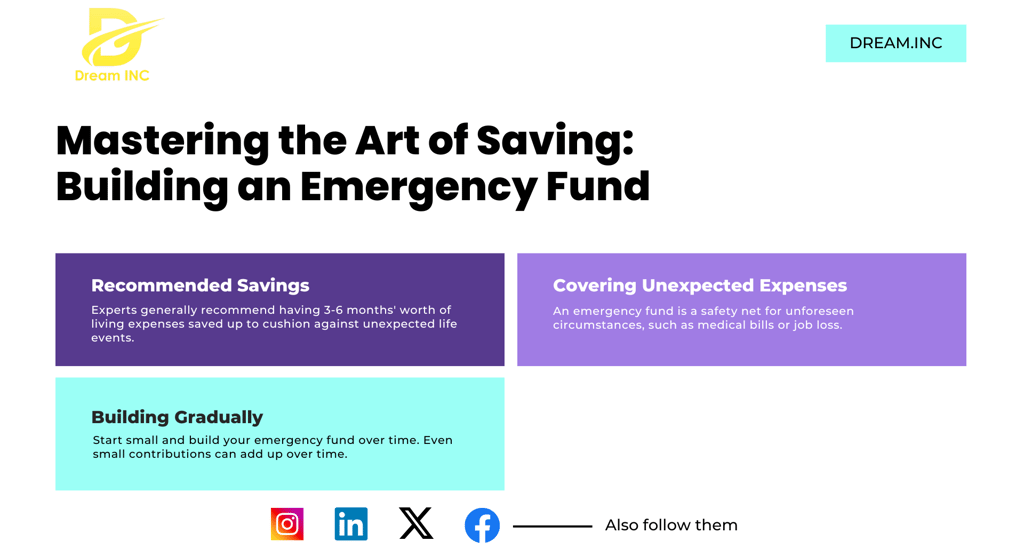

Step 4: The Importance of Saving

In the journey from debt to dreams, establishing a robust saving strategy is essential for achieving lasting financial freedom. Incorporating savings into one's financial roadmap not only allows for a buffer against unexpected expenses but also helps in building wealth over time. An emergency fund, typically three to six months' worth of living expenses, serves as a financial safety net, protecting individuals from the impact of unforeseen circumstances such as job loss or medical emergencies. Setting aside a specific amount each month can gradually accumulate this fund, providing reassurance in times of need.

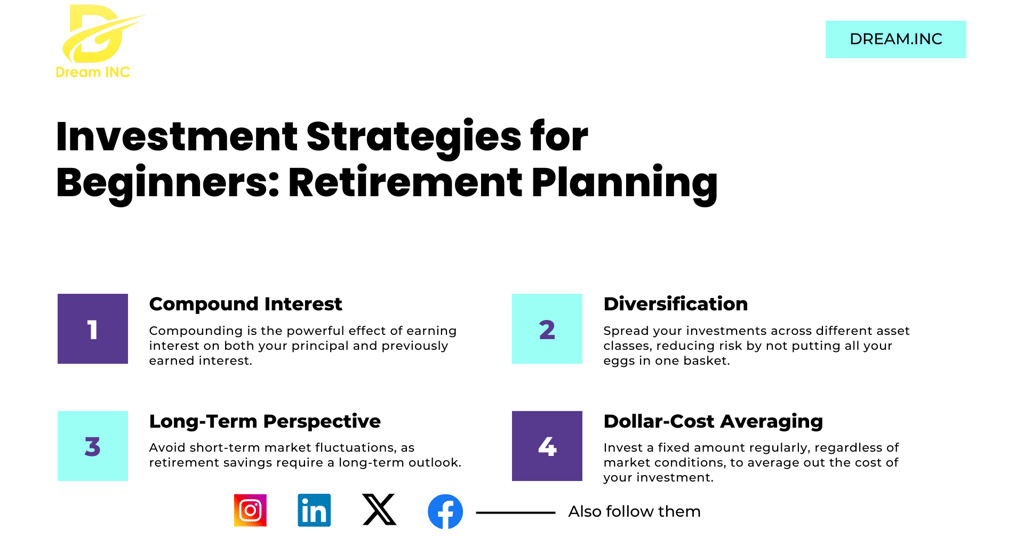

In addition to preparing for emergencies, retirement savings play a pivotal role in long-term financial health. Opening retirement accounts, such as a 401(k) or an IRA, enables individuals to invest for their future while taking advantage of tax benefits. Regular contributions, even if modest, can compound significantly over the years, ensuring a more secure retirement. Incorporating employer match contributions, if available, is another strategy that maximizes savings potential and accelerates progress toward financial goals.

Cultivating consistent savings habits is also crucial. Automating transfers to savings accounts can help eliminate the temptation to spend, promoting a disciplined approach to savings. Setting specific financial goals, whether for a vacation, home purchase, or other aspirations, can motivate individuals to save diligently and track their progress effectively. Furthermore, the psychological benefits of saving cannot be underestimated. Having savings contributes to a sense of security, reducing financial stress and fostering confidence in one's financial standing. This sense of empowerment can inspire individuals to make smarter financial decisions, ultimately paving the way for the realization of their dreams.

Step 5: Investing for the Future

Investing is a crucial component of building wealth and achieving long-term financial goals. Understanding the different types of investment vehicles available can empower individuals to make informed choices that align with their financial aspirations. Among the most common options are stocks, bonds, mutual funds, and real estate. Each of these has unique characteristics and varying levels of risk and return, which investors should evaluate based on their personal financial situations.

Stocks represent ownership in a company and can offer significant growth potential. However, investing in stocks comes with volatility and risk, making it vital for individuals to assess their risk tolerance before committing capital. Bonds, on the other hand, are considered safer investments, essentially loans made to corporations or governments in exchange for fixed interest payments over time. Understanding both stocks and bonds will help investors craft a diversified portfolio that can weather market fluctuations.

Mutual funds allow individuals to pool their money with others to invest in a diversified selection of stocks and bonds, making them an attractive option for those who prefer a hands-off investment approach. Real estate is another avenue that not only offers potential income through rentals but can also appreciate in value over time, adding to an individual's wealth over the long term.

As you embark on your investing journey, it is essential to establish clear investment goals. Whether saving for retirement, funding a child's education, or buying a home, clearly defined objectives will help guide your investment choices. Additionally, consider starting with a small investment and gradually increasing your contributions as you become more comfortable with the process.

In conclusion, viewed through the lens of risk tolerance and investment goals, investing is a powerful strategy for transforming financial dreams into reality. By leveraging the knowledge of various investment vehicles and beginning with a clear plan, individuals can enhance their financial freedom and pave the way toward a more secure future.

Step 6: Planning for Insurance and Risk Management

In the journey toward financial freedom, it is crucial to incorporate risk management strategies that protect against unforeseen events. Insurance serves as a vital safety net, serving to mitigate the financial impact of unexpected circumstances such as illness, accidents, or property damage. Various types of insurance are available to consumers, including health, life, disability, and property insurance, each designed to address specific risks and provide financial security.

Health insurance is essential for covering medical expenses, ensuring that individuals can seek necessary medical care without incurring debilitating costs. With rising healthcare expenses, obtaining a comprehensive health plan is a critical component of financial planning. When assessing your health insurance options, it is imperative to compare plans based on coverage limits, premium costs, deductibles, and out-of-pocket maximums to identify the best fit for your needs.

Life insurance offers financial protection for dependents in the event of an individual's passing. This type of insurance can help cover living expenses, debt obligations, and future financial goals such as education for children. When evaluating life insurance policies, individuals should consider their family's financial situation and the amount of coverage needed to ensure their loved ones are secure.

Disability insurance and property insurance are equally important in safeguarding financial stability. Disability insurance protects against lost income due to illness or injury, enabling individuals to maintain their standard of living. Property insurance, including homeowners or renters policies, protects against loss or damage to personal property. It is essential to assess your specific needs for each type of insurance to tailor your coverage appropriately.

Ultimately, the process of selecting and maintaining adequate insurance coverage requires careful evaluation and thoughtful comparison of policies. By securing appropriate insurance, individuals can navigate the path to financial freedom with greater confidence, knowing they have an effective risk management plan in place. This strategic approach not only protects against potential financial burdens but also lays a solid foundation for achieving long-term financial stability.

Your Ongoing Journey to Financial Freedom

Achieving financial freedom is not merely a destination but rather an ongoing journey that involves continuous assessment and refinement of one’s financial plans. As one progresses along the path toward financial stability, it becomes imperative to regularly revisit and adapt strategies based on evolving personal circumstances. Life is dynamic, and financial goals must be recalibrated accordingly to ensure that they remain relevant and attainable.

Setting new financial goals is essential as you achieve the milestones you initially set. These objectives can range from establishing an emergency fund to investing in a retirement account or saving for children's education. As you achieve each goal, it's crucial to look ahead and define what next steps to take, whether it involves expanding investments, redirecting funds to pay off debt, or even beginning to explore avenues for passive income. By remaining proactive, you cultivate a mindset that prioritizes both short-term gains and long-term financial health.

Additionally, tracking your progress is vital for maintaining motivation and accountability. Utilize budgeting tools or financial apps to monitor spending habits, savings, and investments. Regularly reviewing your budget can provide insights into areas for improvement while reinforcing positive financial behaviors. Moreover, engaging with educational resources about personal finance can equip you with knowledge and strategies that further augment your financial literacy.

Adaptability is a cornerstone of this journey. Economic conditions, personal relationships, and unexpected events such as job loss or health issues can necessitate shifts in your financial approach. Resilience in facing these challenges can mean the difference between falling back into old habits and preserving financial health. Thus, embracing both the successes and the setbacks will ultimately lead to a more profound understanding of what financial freedom means for you personally.

Contact Us

Reach out to us for any inquiries or loan applications.

+91-9310147220